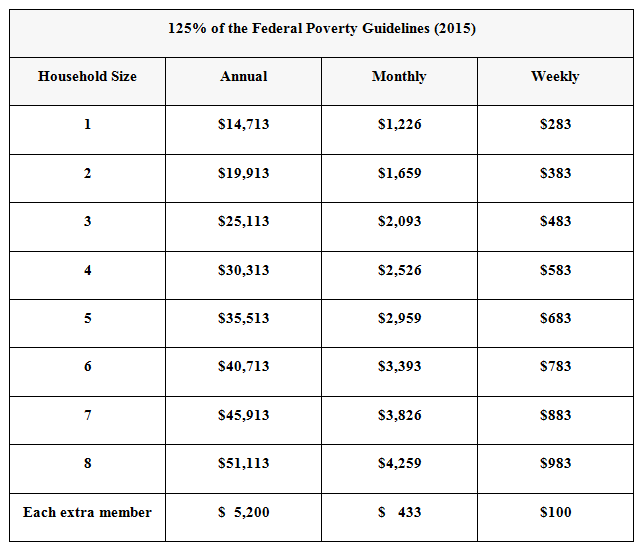

You need to complete this section of the form only if your reported income in Part 6 was less than 125% of the Federal Poverty Guidelines for your household size. Here are those Guidelines for 2015 (they are adjusted each year):

How much is needed?

If your income was not at or above the required level, then you may use financial assets to make up the difference. How much is required? Follow these steps to find out:

- Find the difference between actual income and required Let’s assume that you have a reported household size of 3. Using the chart above, we see the required annual income level is $25,113. Let’s assume your annual income is $20,000. That leaves a difference of $5,113 between your actual income and the required income.

- Identify your relation to the immigrant being sponsored. The amount of required assets will depend on your relation to the person who is immigrating. For most immigrants, you will need to demonstrate assets that are five times the difference you identified in step one. But if the person being sponsored is your husband/wife or minor child, then you have to show only three times the difference. Also, in certain circumstances involving an immigrant orphan the assets need to be only one times the difference in step one (these cases are rare).

- Multiply the amount in step one by the factor identified in step 2. Let’s assume you are sponsoring someone to whom you are not related. This is the most common scenario. In that case you will need to show financial assets five times the difference you identified in step 1. In step 1, we found a $5,113 difference between the actual income and required income. 5 x $5,113 = $25,565. So this means you will need to report financial assets that are valued at $25,565 or greater.

What assets may be used?

The rule for assets is that they must be “available in the United States for the applicant’s support and must be readily convertible to cash within one year.” What does this mean? That you are allowed to count an asset only if you can sell it, and have the resulting cash in the U.S., within 12 months. So obviously the ideal assets would be money in a U.S. bank account, since that’s U.S. cash that’s immediately available. But it is common for joint sponsors to need to rely on other forms of assets, and these require some more careful assessment. Types of assets may include stocks, bonds, certificates of deposit, and property (both real estate and other forms of property).

Documenting the asset. You are required to provide the following documentation for any asset you report in Part 7:

- Proof of ownership.

- Proof of where the asset is located.

- Proof of the date you acquired the asset.

- A 12-month withdraw history.

- Proof of valuation (if applicable).

This documentation generally does not need to be notarized. In the case of a checking account, for example, you may simply provide copies of your last 12 months of statements to satisfy all requirements above. Issues with proof of valuation are most common when real estate is used. Ideally a recent appraisal of the property would be provided. Since this is expensive to obtain, sponsors often submit alternative evidence instead, such as tax assessment records and a free valuation from an online real estate site such as Zillow.com. Such alternative evidence may not be accepted by the immigration services, however.

Using assets of a household member.

You may include the assets of another household member (see Part 7, item 5), but only if: (1) the household member completes a Form I-864A; and (2) the household member has been living with you for a minimum of 6 months. The household member’s assets need to be documented for the Form I-864A in the same way described above. You should also present proof that the person has been living at your address for the required 6 months, such as a rental agreement listing the individual, or bills sent to the address with that person’s name.

Using assets of the sponsored immigrant.

You are allowed to count assets owned by the primary sponsored immigrant. Importantly, however, the immigrant’s assets may be counted by only one sponsor. So if you are a joint sponsor, you need to ensure that the primary sponsor has not already reported the immigrant’s assets on his/her Form I-864. If the immigrant’s assets are available for you to report, the immigrant does not need to complete a Form I-864A. But you will need to provide documentation of the assets as described above (showing ownership, etc.).

Using assets outside the U.S.

What if you want to rely on assets in a foreign country? This is theoretically possible, but complex. Remember that the assets need to be available as cash in the U.S. within 12 months, if needed. You would need to provide documentation that it would be possible for you to make this happen, if needed. This would be relatively easy, for example, in the case of a London bank account, and a notarized letter from your banker should be sufficient. But the case becomes far more complex with countries who have less close financial ties to the U.S. For other countries you would be wise to provide a notarized legal opinion statement from an attorney explaining that the assets could be sold and proceeds transferred if needed. For any non-U.S. assets there is a good chance you will receive a time-consuming request for additional documentation from the immigration service.